What I’m Doing with My Money

As I said above, it’s that time again when I pull out the records of all my business and financial transactions over the previous 12 months and take a longish view of all the assets I have, in what categories and in what proportions, think about how they got to be what they got to be, and then figure out how I feel about all that, given the economy and the business environment and the state of the financial markets.

I just reread that last paragraph and I realize it makes me sound like a Type-A brain-breaking financial analyst. I am not. Rather than spend the hundred hours it would take me to research and analyze all the data myself, I rely on the insights and acumen of six or eight economists and investment analysts for whom I have enormous respect and confidence because I’ve been working with them and seeing the results of their work for nearly 40 years.

What I do in preparation for this annual report, then, is have Gio print out all of the financial statements from all of my passive investments and all of the P&Ls from all of my businesses, and then ask my three boys, each of whom now manages these various projects, businesses, and investments, to write summary accounts for me in language I can understand.

That usually prompts concerns and questions that I talk to them about and then, if needed, run by one of my six trusted financial advisors, including Dominick, my stockbroker, and Sean, my partner in several investment and wealth building publications, and then, based on all that, decide what I’m going to leave as is (which is usually most of it) and what I should change.

I realize that many of those reading this now will be thinking, “I don’t care about all that, Mark. Just tell me what you are doing with your stock portfolios. Are you buying? Are you selling? Are you changing the balance of assets? And if so, why?”

Those are fair questions. And I mean to answer them. But I want to give you an answer that is more important than telling you what I’m doing with my stock accounts. I want to talk about all the major asset classes I invest in. I want to tell you exactly what I’m doing to preserve my wealth and perhaps bring it up a notch or two before the end of this year.

It’s Not About Stock Investing. It’s About Building Wealth.

I started writing about “money” in 2010, when I began writing essays for a new digital publication called Creating Wealth.

Creating Wealth was intended to be my version of an investment advisory newsletter – which most people would expect to be my advice about investing in stocks. But since very little of my wealth came from stock investing, and since the stock investing that I did at the time was limited to a single index fund, I didn’t have much to say about it. I did, however, have plenty to say about all the other financial assets that had been the primary generators of the outsized income I made that grew my wealth.

Stocks and bonds are certainly a part of what I call my Wealth Portfolio, but just a part. A bigger part is comprised of income-producing real estate, rental properties that I control and oversee. An even larger portion is in private equity – often in businesses that I started and/or funded in the past. I also have a sizeable portion in private debt. And another portion in collectible assets such as rare books and fine art. And I own a bunch of gold and silver, some rare coins, and a basket of cryptocurrencies (even though I’ve never been a believer in the long-term potential of cryptos).

Isn’t that just too much?

Wouldn’t it be easier to stick with stocks and bonds?

Yes, that’s a lot of different financial assets. And yes, it would be easier if, like most investors, I invested solely in stocks and bonds.

The reason I don’t is mostly because that is not how I got rich.

Let’s Talk About Stocks and the Stock Markets

I am not a stock picker. Never was. Never wanted to be. But I’ve worked in the C-Suites of the financial advisory publishing world for more than 40 years, and I’ve learned enough to know dozens of ways to lose money with stocks.

I know, too, what anyone who has studied stock investing and/or the history of the stock market knows: It’s difficult to achieve an overall return on a stock portfolio that is better than the historical ROI on stocks, which has been about 9% to 10% over the last hundred years.

Difficult but not impossible. It can be done. It can even be done without taking imprudent risks. I’ve done it. But I’ve gotten considerably better returns from other investments. In fact, over the years, stocks have represented less than 15% of my net investible wealth.

That said… What am I doing with my stocks right now?

When I began to write about money-making strategies for Creating Wealth, I had all of my own “stock” money in an index fund.

But since so many of the subscribers to Creating Wealth were interested in individual stocks, I felt an obligation to do something more than just mention the fund I had invested in. So I decided to create my own model stock portfolio for my readers, based on Warren Buffett’s investing ideas. I brought together some of the best stock analysts I knew and asked them to help me build a model portfolio that would represent “what Buffett would buy if he were starting Berkshire Hathaway today.”

When it was completed, we had a model portfolio made up of big, safe companies with significant competitive advantages. (I believe Buffett calls them “moats.”) I called it the Legacy Portfolio, because all of the stocks in that portfolio were meant to be held more or less forever. I invested in them myself – and I held on to them. That’s why my answer to the question of what I’m doing each year with my stocks has usually been “nothing.”

This year, however, I’m going to be making some major changes to the portfolios in three of my five Legacy accounts.

What changes am I making? And why?

I have rarely made investment decisions based on what I think will happen in the future – either with the global economy, the US economy, or even in industry sectors.

There are some financial analysts who have been able to warn their clients/subscribers of upcoming major market shifts and give them opportunities to profit from them. But having been in the financial advisory business for more than 40 years, I can tell you that these people are rare. And even the best of them, at one point or another, miss the mark.

Given what I know – and especially what I know about what I don’t know – I have always taken their individual predictions and recommendations as significant but imperfect considerations in making the ultimate decision, which must always be mine.

But when they (not the general population of prognosticators but the half-dozen I trust and respect) are all worried about the same thing, I tell myself that it would be foolish of me to ignore them – and I see if there are some adjustments I can make in the way I’ve allocated my financial assets that (1) would not be an abandonment of my core investment strategy, and (2) would, at the same time, insure and/or leverage my portfolio based on the assumption that they might be right.

Around 2004 and 2005, for example, it became clear to me that the real estate experts I trusted had become bearish while the market was heating up. Since my approach to rental real estate investing is very conservative (in the same way that my approach to stock investing is), I didn’t feel the need to sell any of the properties I owned. But I did desist from buying new properties until after the 2008 crash when those that were coming to market were very, very cheap.

On the leveraging side, in 2017, although I believed that cryptocurrencies had no long-term chance of survival, I bought five coins each of Bitcoin, Litecoin, and Ethereum as a hedge when the price of Bitcoin was hovering around $1,000.

And in the early 2000s, I was finally persuaded by a consensus of the conservative economists I read that there was good reason to start buying gold. I began slowly, buying Canadian Maple Leafs and then South African Krugerrands. And I continued buying until about 2005 for an average price of about $400 a coin.

As far as stocks are concerned, I’ve been strict about not fiddling with my Legacy portfolios on a year-to-year basis. But every three or four years, I may adjust them in a minor way by removing the stock of a company whose business model has drastically changed or adding shares of a company or two that either Sean or Dominick has convinced me should be added.

And that’s what I’m doing this year. Sort of…

My two main concerns: debt and current market analytics

I am not an economist. Nor am I a market analyst. I don’t have the mind for that sort of slow and careful thinking.

What I do to compensate for my lack of expertise in those two areas is to follow about a half-dozen economists and stock market analysts that I know (from working with them for decades) have proven instincts when it comes to dangers and opportunities in the markets.

In terms of economics, the big concern they all have is debt. Primarily US government debt that is now north of $36 trillion. But also commercial debt, student debt, and consumer debt.

They are convinced that the US cannot sustain this level of debt. And I haven’t read a counter argument that is convincing.

This I do know about economics: National debts are always repaid – one way or another.

One way is through a major depression. Another is through hyperinflation – an extended period of high inflation. And the third is by an extended period of massive GDP growth.

Trump is counting on option three. And although I have hope that some of his executive orders – decreasing regulation, lowering taxes, and using tariff threats to bring foreign businesses back to the US and lower tariffs overall – will work, I don’t see it happening in the next three to five years.

Either one of the other two options – a major depression or hyperinflation – is likely to bring the stock market down in a big way. And my limbic brain is telling me the meltdown is going to happen in the not-too-distant future.

As far as market analytics go, I have another worry. The current P/E ratio of stocks in the major indexes stands at 30. That means investors believe that these companies are valuable enough to merit selling their shares for 30 times earnings.

Would you spend $3 million on a landscape company whose annual profits are only $100,000?

I wouldn’t.

The bottom line: I believe there is a fair to good chance that we will see the stock market take a 30% to 50% tumble in the next five years.

That is not necessarily a fear that would prompt me to sell any of the stocks in my two core Legacy portfolios. Those decisions I will leave to the two experts who manage my two Legacy accounts: Dominick and Sean.

But for the three Legacy portfolios that fund my family’s three non-profit enterprises, I am inclined to take steps immediately to safeguard those portfolios from such a correction. I’m considering trading some of the shares I have in stocks like Nvidia, which have done so well for me in the past few years, to shares of bread-and-butter companies that will likely be less affected by a 30% to 50% drop if it happens.

Why am I doing that?

I’m doing it not because I have lost trust in the long-term viability of the Legacy portfolios. On the contrary, for my personal accounts, I’m leaving them just as they are.

But these endowment accounts have a second financial purpose that my personal accounts don’t have. They are meant to increase their value over the long run, but they are also meant to pay for the current expenses of the non-profit entities. For the past many years, I’ve been confident that they could do that because they could cover those expenses with a distribution of less than 4% of the account balances every year.

The account we have for Fun Limón, for example, the community center our family foundation sponsors in Nicaragua, is about $8 million. The cost of running that operation is about $250,000 to $300,000 a year – or 3.5% to 4% of the balance.

Based on industry standards, if I can keep the distributions from these accounts to those levels, I shouldn’t have to worry about the endowment shrinking. A distribution of 3% to 4% has proven to be low enough to avoid a situation where the principal is in danger.

And since I get five-year government bonds with yields of about 4.5%, I wouldn’t have to worry about a market crash and seeing that $8 million drop to $5.5 million or even $4 million, which would mean that I would be forced to spend down the principal at the worst possible time.

Knowing that I can keep the account at $8 million for the next three to five years without any exposure to market risk feels like the right move to make, given the purpose of these funds.

At least that’s what I’m thinking now. I’m going to speak with Dominick later today and see what he has to say. If there’s something wrong with my thinking, he’ll point it out to me, and I’ll pass that on to you next week. But for the moment, that’s my plan.

Important: I’m not dumping the stocks in my personal accounts. Here’s why…

As I mentioned above, I’m not going to ask Dominick or Sean to lighten my stock holdings in my two Legacy accounts. I’m going to do what I’ve always done – with good results. I’m going to let them make those decisions.

This has worked since I established those accounts – and that’s because the stocks in the Legacy portfolios were designed to withstand the test of time, to continue to become more valuable over the long haul, regardless of market fluctuations. They were set up in response to my desire to build a portfolio of the kind of stocks that Warren Buffett would buy if he were getting into stocks for the first time.

As for what Dominick does within my personal Legacy accounts, he is always making minor adjustments to optimize the ROI. When a single stock hits 10% of the value of the portfolio as a whole, he shaves some of it off the top and puts it into other Legacy stocks whose pricing is attractive for the time being. He also sells puts and does covered calls to increase the cash flow. These are the two safest ways to use options in a stock portfolio that I know of, and since Dominick is very good at doing it within the guidelines of my conservative mandates, I can let him make these adjustments at will. That has improved the overall performance of the portfolio by 10% to 20% over the past five years.

Now let me tell you what I’m doing with the other parts of my Wealth Portfolio.

My Investments in Rental Real Estate

I’ve been investing in real estate since 1981, but it wasn’t until 2007 that I figured out how to make it work.

Well, that’s wrong. I didn’t figure it out. My brother did. He quit his job that year and put all his time and money into building a real estate empire.

These days, I’m looking for individual rental properties that I can buy for about 100 times the monthly rent roll. When I used to buy single-family homes, for example, I would pay up to $200,000 for a house that I could easily rent for $2,000 a month. Today, I’m on the lookout for larger properties – apartment buildings and offices – that I can get for the same cost/rent ration. If I can find an eight-unit apartment building that generates $12,000 a month in rent, I’ll be interested in buying it if I can get it for about $1.2 million or less.

(This is, admittedly, a rough calculation that gives me an initial indication of the value of the deal. Before I commit to buying a property, I ask whoever I’ve chosen to manage it to dig deep into the numbers to make sure there are no hidden surprises on the cost side or no significant risks of deflation on the income side.)

By taking this approach, I don’t have to worry about the larger countrywide real estate market, the way I would if I were investing in some of the larger, more reliable REITS. I simply look for the deals. And if I can’t find them, I hold on to my cash.

Right now, in the local real estate ponds I fish in, I haven’t been able to find anything that meets my criteria. So I’m not buying anything. But if something comes along – this year or next year – I will.

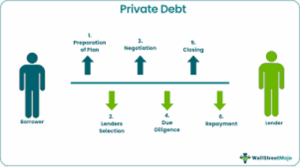

My Investments in Private Debt

Between 1987 and 1995, I went in with my former partners who had started a business that was in the business of lending money – writing loans for private individuals and companies that had significant assets that were to some degree illiquid, in return for interest rates considerably higher than they could get with, say, government bonds.

The range of debt they were financing ranged from used-car loans, to short-term business loans secured against receivables, to financing commercial receivables, and to buying out life insurance settlements and lottery claims.

The ROIs they were getting from those investments ranged from 15% to 20%. That was three to four times what I was getting from municipal bonds, and better even than I was getting from my rental real estate properties. I remember thinking, “Why doesn’t every investor do this?”

I eventually found out why.

When my partners set up those deals, they felt that we had full control over how much we were willing to lend and on what terms and at what rates.

Let’s take, for example, the deals we were making with lottery winners. These were individuals that had won multimillion-dollar prizes, but the money was going to go to them over many years. We could offer to pay them, say, 75% of the total amount, pocket the 25%, and be confident that we’d get paid off by the state in full and on time because no state was going to risk destroying its lottery income by defaulting on a payoff.

But financing used cars is considerably riskier because the people that need to borrow money to buy a used car are usually doing so because they don’t have the creditworthiness that cash buyers have. Their net worths are usually small or even negative. Which means that if they default on the loan, there’s very little the lender can do about it. The lender could, of course, sue for the money. But the chances that such a suit would be financially feasible are depressingly small.

That is the primary reason why this sort of lending is rarely done by big institutions and why the smaller lenders that get into it tend to charge much higher rates and establish contractual demands that are much tougher than what is “normal” for a loan.

So, on the one hand, this sort of lending will usually produce higher (sometimes considerably higher) ROIs. On the other hand, private lenders, despite measures taken to protect themselves, are always taking on more risk.

The safeguards my partners had installed worked well during economic good times. But when the economy slowed and made it nearly impossible for our type of borrower to pay back their loans, the defaults shot up far higher than our most aggressive expectations.

The same principal holds true for my investments in private debt. I could, if I knew something about public companies that engage in private lending, find a stock or two that would emulate the market. Or I could invest in banks if I knew what was going to happen to them. When our family foundation makes loans to private individuals, we follow a strict protocol that is not dependent on guesses about the future of the economy or the banking industry or even the private debt industry. It is based solely on facts: Does the borrower have enough collateral to back the loan 100%, and will we get an ROI on the loan that is worth getting?

In other words, private debt, like rental real estate, is best used in an active way, by investing in one deal at a time with people you know and trust. One could invest in a public company that makes a profit that way, but the risk there is so much greater because you are two or three steps removed from the individual borrower.

My Investments in Private Equity

Private equity investing is buying and/or owning shares of private (i.e., non-public) businesses. It’s the active equivalent of investing in stocks.

There are two very important differences, however. One is that to be successful as a private equity investor, you need to know a lot more about the companies you are investing in than you do when you are investing in stocks. The other is that if you know what you need to know about the businesses you invest in, you can make a lot more money with private equity than you can by investing in public companies on a stock exchange.

How much more?

Way more. Way, way more. Like turning a $15,000 investment into $15 million over 15 years.

That said, I don’t recommend private equity investing as a realistic way for ordinary investors to build wealth. And that’s because the odds of getting richer this way are extremely poor.

Unless…

Unless, like me, you have had the opportunity to work in an industry for many years and at a high level, giving you an “inside” perspective on that industry that you truly understand and can use to invest in it as an insider.

This is, admittedly, a high fence to climb over. But I believe, based on 40 years of making mistakes and making profits, that it is a fence that should be high. Jumping over little obstacles to take a chance at getting rich is basically gambling. And the only people that get rich in the game of gambling are the people dealing out the cards.

If you are wondering whether I would “greenlight” you to invest in private equities, measure your own experience against my 5 rules:

My 5 Rules for Not Losing Money in Private Equity

1. Don’t invest in businesses unless you understand them from the inside out. And by that I mean: Invest only in businesses that you have been personally involved in, at a senior level (CEO, CMO, Growth Strategist) for at least 10 years.

2. Invest only in businesses that are run, or are going to be run, by someone you know and trust. In other words, people that you have worked with as a colleague, mentor, or competitor for at least five years.

3. In negotiating your investment contract, make sure it gives you some degree of say about the major decisions of the business and make sure the CEO and other key people are comfortable with that.

4. Make the agreement a win-win for both sides. Since you know the business as well as or better than the person who will be running it, make sure that he/she is properly treated and compensated to avoid problems later.

5. Be prepared to take a role in the business that will almost certainly be more active than either you or the current CEO thinks it will be when the contract is signed. And that includes having difficult discussions and making tough decisions when needed. Ultimately, you and the CEO must agree that the purpose of the business is not to line your pockets, but to build a trusted brand and grow its net revenues in a way that ensures it will be around for a long time.

Fine Art & Collectibles: What I Own and Why I Own It

By collectibles, I mean fine art and artifacts that tend to appreciate in value over time. What I like about collectibles is that (1) like real estate, the arithmetic of investing in them is not difficult, and (2) I get to use and enjoy them while their value grows.

I now have a number of collections, each of which has appreciated nicely, and all of which I regularly enjoy.

I have about a dozen rare first-edition books by writers I admire (Mark Twain, William Faulkner, Ernest Hemingway, et al); about a hundred rare gold coins; a half-dozen watches, two of which are worth their weight in gold – literally; and several Greek and Roman vases.

But my primary investment in collectibles has been in fine art, museum-quality art – important pieces that will almost certainly become more valuable as they age. My intention is for my main collection in this category – a pretty extensive collection of Central American modern and contemporary art – to end up in a museum after K and I die, and I have started to take steps to make sure this will happen.

I’ve written lots about my experiences as an investor in collectibles. I’ve told my stories of success and failure. Collecting art and artifacts can be a very risky business if you don’t know what you are doing. When I began, I knew absolutely nothing, so it won’t surprise you to know that I made every mistake in the book.

But I started in my early 30s, when I didn’t have that much money to invest, so my losses were bearable. And by the time my disposable income was large enough to make big mistakes, I had the experience to avoid them.

My 6 Rules for Investing in Collectibles

1. Practice. Before you start investing real money in real collectibles (i.e., stuff that will appreciate in value), buy at least 100 inexpensive “objects” that appeal to you in some way at flea markets.

2. Specialize. And Specialize. And Specialize. Start with one general category that interests you and keep narrowing it down. Let’s say you are interested in antiques. Narrow that down to European antiques, then 19th century European antiques, then 19th century French antiques, then 19th century French armoires… and so on.

3. Buy Authentic. The collectibles industry is riddled with fakes. At the beginning, buy only from dealers and auction houses that guarantee authenticity.

4. Buy Rare. Whether you are collecting art, antiques, cars, rare coins, or whatever, the same rule holds when it comes to ROI: rarity is king.

5. Give Preference to What Is Coveted. Next to rarity, the biggest factor in price appreciation is dictated by authority – i.e., the period or style of the object that is considered by experts to be the best in its class.

6. Pay Attention to Condition. Once-damaged and now-restored pieces can still be very valuable, but those in perfect (or near-perfect) condition are usually a better investment.

My Investments in Cryptocurrencies

Yes, I have some money in cryptocurrencies. And yes, their current worth is considerably more than my investment. But I’m not buying any more because I believe they will one day be made illegal and confiscated by our government. That will happen after our government issues its own “stable coin” – a digital dollar that will be an inflatable currency just like the paper dollar, as well as another high-tech tool to monitor our daily business and personal activities and track every dollar we make and spend.

You might be thinking: “Mark, if you believe that’s going to happen, why did you buy those coins in the first place?” And the answer, to be honest, is that if it turns out I am wrong about my dystopian prediction, I can still say, “Yeah, I bought crypto early and made a killing on it.”