My 100-Day Report Card for Donald Trump

Trump’s Second Term: Not a Sequel, a Reboot

As I mentioned in the introduction to this issue, writing my “report card” on Trump’s first 100 days in office turned out to be a much bigger challenge than I had anticipated.

Researching the promises made and actions taken was not difficult. What I did not expect was how many promises I’d have to research. As you will see as you read (skim?) through this, Trump’s campaign consisted of an almost endless string of complaints about what the Biden administration was doing wrong, and an equal number of promises to set those errors right.

Thinking about how Trump went about business this year as compared to 2016, the unprecedented number of executive orders he has signed so far was predictable, given both the number of pledges and promises he made and the diversity of issues he covered.

It’s also clear that at least half of the orders he signed were historical firsts – declarations and decisions the likes of which I don’t remember prior presidents making, such as renaming the Gulf of Mexico, banning CRT from being taught in public grade schools, and declaring that there were only two sexes.

But I don’t fault Trump for that. I praise him for it. The political and ideological insanity that took place in government, academia, and media after Biden took office was absolutely mindboggling. A toxic mix of very stupid ideas exacerbated by an epidemic of Trump Derangement Syndrome (that affected nearly half of the voting population) transformed our political and social culture to something that I had believed could only exist in science fiction.

So yes, someone had to be, as they say, “the adult in the room” and say, “No, gender is not a spectrum. It is a binary. And no, race is not a binary. It’s a spectrum. And no, claiming to be a victim doesn’t make you a victim. And even if it did, that would not give you any right to demand compensation for it.”

Trump made so many promises during the campaign because there were so many things going on that were divisive, damaging, and dangerous. His election, winning the popular vote, capturing all the swing states, and improving his numbers with Hispanics, Black men, and young voters was a call for a return to common sense.

So, now you have my view on why Trump got so busy after Jan. 20. What follows is an attempt to look at what I thought were the most important issues about which he made promises and compare those promises to what he’s done so far to keep them.

Because of the number of promises I’ll be covering – and about issues that are not just important but strongly debated – I’m going to ease into this by starting with a promise that probably was the least important in terms of current and future affairs but has been eagerly anticipated almost universally. I’m talking about Trump’s promise to let us all see what is in the Kennedy assassination and Jeffrey Epstein files.

Make America Transparent Again

During his 2016 campaign, and again in 2024, Trump strongly implied that he would open long-classified government files – especially those related to the JFK assassination and Jeffrey Epstein.

This was a promise, I was thinking, that could be kept on Day One of Trump’s term. It certainly was a lot simpler than, say, draining the swamp or ending two raging wars.

Some files have been released. But where are the bombshell discoveries that were teased (and that I was, admittedly, hoping for)?

What’s Actually Been Released?

Some progress has been made.

In 2017, during his first term, Trump did approve the release of thousands of documents related to the Kennedy assassination. But under pressure from intelligence agencies, he also allowed key redactions and delays. By 2021, over 90% of the JFK files were technically public, but many pages remained heavily redacted. A 2023 tranche under Biden did release additional pages – but even then, the most sensitive files remained sealed on national security grounds.

As for Epstein, the most recent major disclosures – the unsealing of names from his 2015 defamation suit – were court-driven, not part of a Trump initiative.

Despite Trump’s past association with Epstein and his claims that he “knew things” and would expose the network, no presidential order or DOJ-led transparency effort has yet materialized.

What’s Still Hidden?

* The JFK Files: According to the National Archives, as of late 2023, several thousand documents remain partially or fully classified. Some are believed to contain information about CIA operations, possible Cuban or Soviet links, or domestic surveillance activities that may still be deemed too sensitive – or embarrassing – to disclose.

* The Epstein Case: The FBI, DOJ, and other agencies still hold a mountain of sealed files, including evidence gathered from Epstein’s properties, communications with high-level figures, and testimony from alleged victims. None of this has been voluntarily declassified by any administration.

Success Grade: D

Effort Grade: D

Messaging Grade: F

To be fair, Trump is not the first president who has not kept his promise on this issue.

Who’s Done More to Declassify? A Quick Comparison

Donald Trump

* The JFK Files: Authorized large-scale release in 2017 but delayed full declassification at the request of intelligence agencies. Some additional files released in 2018.

* The Epstein Case: No formal effort to declassify or release files. Occasionally made public comments suggesting knowledge of the case, but no action taken.

* Other Transparency Promises: Vowed to release documents on 9/11 and other “Deep State secrets,” but most remain sealed.

Joe Biden

* The JFK Files: Oversaw release of additional batches in 2021 and 2022. In Dec. 2022, the White House announced that 95% of JFK documents were now public – but watchdogs noted that the most sensitive documents remain redacted.

* The Epstein Case: No initiative to release classified government files. The 2024 unsealing of names came from civil court rulings, not the executive branch.

Barack Obama

* The JFK Files: No significant action taken during his administration.

* The Epstein Case: No known effort to release or unseal documents.

* Other Transparency Promises: Campaigned on transparency in 2008 but faced criticism for prosecuting more whistleblowers than all prior presidents combined and for expanding state secrecy in areas like drone warfare and surveillance.

Conclusion

Despite early rhetoric, no modern president has fully “opened the books” on either JFK or Epstein. Trump arguably went furthest with the JFK files – but even he fell short of full disclosure. The Deep State, it seems, still knows how to keep its secrets.

Now let’s move to a promise for which I gave Trump high grades – because he did exactly what he promised and what he promised was and is a very necessary thing.

Make the Southern Border Secure Again

What Trump Promised

From the moment he launched his second campaign, Trump made it clear that immigration would once again be a central pillar of his presidency.

This time, however, his goal wasn’t just to stop new waves of illegal migration – it was to reverse what he described as an unprecedented invasion allowed (and encouraged) by the Biden administration.

He promised to “shut the border,” reinstate the policies that had worked in his first term, and go further by deporting the millions of undocumented migrants who had entered the country since Biden took office.

He also vowed to bypass the bureaucratic entanglements that had previously slowed immigration enforcement, saying he would “end the invasion” through direct executive action and tougher mandates on federal agencies.

What He’s Done

Within days of taking office, Trump issued a sweeping executive order rescinding Biden’s border enforcement rules and reactivating the policies his administration had used during his first term. That included:

* Reinstating the Remain in Mexico policy for asylum seekers.

* Ending catch-and-release, replacing it with rapid expulsion protocols.

* Expanding funding for border wall construction, using previously authorized (but unspent) funds.

* Re-deploying ICE and Border Patrol with new rules of engagement – specifically lifting internal limitations that had prevented them from detaining or deporting many categories of illegal entrants.

The results have been dramatic. According to DHS data released in mid-April, illegal border crossings have dropped by over 90% since January. Some sources close to the administration say the actual figure may be closer to 97–98%, though that includes seasonal variation and changes in migrant routes.

Trump has also launched Operation Homeland Recovery, a new directive tasking ICE with locating and removing as many of the 12 million undocumented immigrants who arrived under Biden as logistically possible. The operation has already sparked legal resistance from sanctuary cities and lawsuits in several Blue states – but the White House is moving forward regardless, citing public safety and national sovereignty as the justification.

What Biden Did – and Why It Matters

To understand the magnitude of what Trump is trying to reverse, it’s worth stating plainly: The Biden administration’s immigration policy wasn’t just lax. It was immoral and illegal.

Rather than securing the border or working through Congress, Biden used a patchwork of executive orders to dismantle every major Trump-era control. He neutered border enforcement, ended the Remain in Mexico policy, abandoned Title 42 protocols, and instructed CBP to release illegal entrants with mere notices to appear – often years in the future.

Worse, the administration secretly transported hundreds of thousands of migrants via government-chartered flights to small towns and cities across America – often at night. These communities received no funding, no advance notice, and no say in the matter.

The strategy was political: to flood Red and Purple states with future voters who, once given a path to legal status, would likely vote Democrat.

If true, it’s not just a breach of immigration norms – it’s a subversion of the democratic process by demographic manipulation.

What It Feels Like

Trump didn’t just promise to fix a broken system. He promised to stop what many Americans (me included) see as an immensely brazen and immoral violation of one of Biden’s primary responsibilities by not just allowing but encouraging more than ten million unvetted immigrants to cross into the US during his term of office, and then abetting them by flying and busing them throughout the country, under cover of night, without even notifying the affected governors – all in the hope of tipping the balance of future voting irreversibly towards the Blue.

Why nobody pointed this out from day one – with only rare exceptions from conservative pundits – I could not, at the time, understand. But now, seeing it again from how crazy the embraced values were back then, how far they were from common sense, and how widespread the willingness was among the media to suppress the obvious truths, I have to think of it as an era of absolute irrationality driven by TDS, which was too strong and too widespread to stop.

I’m confident that when economists check the federal government’s tab since 2016 – both in terms of spending dollars it didn’t have and destroying wealth it did have – they will see that of the dozens of ideas and actions taken during those eight years, the two worst and most costly were locking down the economy during COVID and opening up the border.

And that is why I give Trump his best grades for keeping this promise.

Success Grade: A*

Effort Grade: A

Message Grade: B

Illegal crossings have collapsed. Enforcement is back. And for the first time in years, the border is being treated like a border.

The asterisk is there because although Trump has fixed the “invasion” problem, he hasn’t yet addressed the larger immigration problem, which is that the US needs immigrants – probably more than a million of them – every year to keep our economy strong and growing. There are reasonable ways to do this with both permanent citizens and temporary workers. If he doesn’t tackle this second issue, all the force and conviction he’s put into closing the border will amount to nothing.

There is hopeful news on this front. Trump has apparently initiated a “self-deportation” program for illegal immigrants to turn themselves in and get some money and a free ticket home, rather than be apprehended. That’s not the interesting part. What I’m excited about is that he said that those who do self-deport will be put on a “short list” to come back with a legal path to citizenship.

Next on the agenda is Trump’s promise to take a hard position on violent and gang-related crime in the United States, which shot up sharply during the BLM protests and is still alarmingly high in many cities across the country.

Make America Safe Again

What Trump Promised

During and after the start of the BLM movement in 2013, there was a significant rise in crime in the United States – and particularly in high-population Blue cities.

Aware of the potential voting points of this, Trump made crime one of his primary examples of how America was moving in the wrong direction and blamed it on the Biden administration. He promised, more than once, that he would “fix it” when he became president.

But it was not just the crime associated with urban riots that he spoke about. There were several social and political “movements” that had taken root in universities and among liberal think tanks that took the position that criminal arrests and convictions should result in ratios that corresponded to racial representation in the general population, that “disadvantaged” minorities should be treated with special consideration (i.e., more leniency) because they were disadvantaged, and that America’s justice system and prison system were systemically racist.

Thanks to leftist funding (most notably George Soros), these movements took hold in many Blue states and cities, with judges and DAs openly easing sentences for criminals and reducing crimes such as theft to misdemeanors, and with Democratic politicians making excuses for the hundreds of millions of dollars of public and private property that was destroyed during the BLM riots (though they were outraged by the Jan. 6 protest, where there was negligible property damage).

All this made it easy for Trump to criticize this obviously idiotic view of crime and criminality and to cast the blame on Woke politics – starring Joe Biden.

And it was not just the vilified White men who were encouraged by Trump’s criticisms and promises, it was Blacks and Hispanics, many of whom had to live through this chaos.

The progressive slant on crime never made a bit of sense – except to academics who wanted to be published in obscure leftist journals. And everyone – including most of the undecided voters in swing states and many liberals as well – knew it.

Trump vowed to restore law and order, re-center the criminal justice system around victims instead of offenders, and take federal steps – wherever possible – to reverse progressive criminal justice policies at the state and local levels.

What He’s Done

In his first 100 days, Trump:

* Appointed a new Attorney General with a mandate to support law enforcement, pressure progressive DAs, and bring federal charges when local prosecutors declined to act.

* Reversed Biden-era DOJ guidance that discouraged federal prosecution for lower-level offenses.

* Launched a new DOJ task force to investigate and, where appropriate, override lenient charging practices by state prosecutors in cases involving violence, gang activity, or drug trafficking.

* Increased funding for federal law enforcement partnerships with local police departments through Operation Safe Streets.

* Issued a White House directive aimed at fast-tracking federal action against sanctuary cities that release criminal aliens into the general population.

The most important move Trump made was in appointing serious, law-and-order advocates to lead federal agencies. People who viewed crime not as a social mystery to be endlessly recontextualized, but as a serious problem needing to be solved.

What It Feels Like

There is no doubt that Trump saw his pro-police and pro-law-and-order rhetoric to be good for votes. And that it helped him win.

What he can do about crime as president, however, is another question. Crime, like real estate, is a local enterprise. Cleaning up crime requires tough initiatives, but local ones. The best thing Trump can do to reduce crime in the US – and perhaps the only thing he can do – is to get rid of the bad public thinking that was ever-present during the Biden administration with liberal Democrats and reflected in the mainstream media. You can’t reduce crime by making it easier to commit a crime and making the punishment easier when you do.

Trump’s victory itself was a blow to that kind of thinking. We will see what his top law enforcement people can do to encourage state and city governments to get tough on crime and on criminals. I’m not holding my breath.

Success Grade: B- (so far)

Effort Grade: B

Messaging Grade: B+

Trump has moved quickly and appointed the right people to execute his strategy. When talking with outrage about crime, he appeals to an increasingly large percentage of US voters. But the results of his appointments and his advocacy of tough-on-crime policies haven’t yet materialized. And although this has disappointed voters who believed he would quickly reduce crime in the US, the data so far is looking positive. If he can make significant headway in the next several months, he will have yet another feather to put in his cap.

Let’s move now to energy – an issue that is much more important than most people realize.

Make America Energy Independent Again

What Trump Promised

Energy independence was one of Trump’s most consistent talking points during the 2024 campaign. As always, he blamed the Biden administration for driving up energy prices, restricting domestic production, and making the US more dependent on foreign oil – despite the risks to national security and economic stability.

He promised to reverse those policies immediately. He would cancel EV mandates, end subsidies for unproven technologies, reopen drilling on federal lands, revive coal, accelerate fracking, and make it easier to export natural gas to Europe and Asia.

And most importantly, he said he’d restore US energy independence – a goal he had briefly achieved during his first term.

What He’s Done

In his first 100 days, Trump moved quickly and decisively. His administration has:

* Lifted restrictions on drilling and fracking across federal lands and offshore sites.

* Rescinded Biden-era EV mandates and emissions targets that forced automakers to prioritize electric vehicles over gas-powered ones.

* Reopened leasing for coal mining operations, particularly in Appalachia and the Mountain West.

* Approved liquefied natural gas (LNG) export terminals to supply European allies still cut off from Russian fuel.

* Ordered the Strategic Petroleum Reserve to begin modest refilling – after Biden had drained it to near-record lows in a bid to lower gas prices ahead of the 2022 midterms.

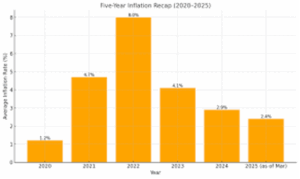

Oil production has surged. Gasoline prices are down. And the cost of natural gas for home heating and power generation has dropped sharply.

What Biden Did – and Why It Mattered

The Biden administration came into office vowing to “end fossil fuels.” It prioritized a rapid transition to renewables, pushed through massive subsidies for EVs, solar panels, and wind farms, and restricted new drilling across public lands.

The intent, ostensibly, was to reduce carbon emissions. But the result was predictable: higher energy costs, reduced domestic output, greater reliance on imports, and a grid that was increasingly strained.

More fundamentally, Biden’s energy policy was based on wishful thinking: that a nation of 330 million people could transition from fossil fuels to renewables almost overnight, without major disruptions or economic fallout.

It didn’t work. Inflation soared. Energy-intensive industries faltered. And American households – especially those in the bottom half of the income ladder – felt the squeeze.

What It Feels Like

I’m not against renewable energy. I’m in favor of it. But what the Green movement has done in the US over the past five years has been irrational and counterproductive.

All economies run on energy. That’s as true today as it was 100 years ago. Reduce an economy’s access to affordable energy, and you reduce its GDP. You reduce productivity. You reduce the standard of living. And the people who get hit hardest are always the ones with the fewest resources.

Transforming an energy system from fossil fuels to renewables isn’t something that can be done quickly without serious economic damage. And if the goal is to lower global carbon emissions, doing it unilaterally is not just foolish – it’s futile. China, India, and large swaths of Africa aren’t giving up coal and oil just to appease Western sensibilities. They’re growing economies, and they’ll burn what they need in order to grow.

Even building renewable infrastructure – solar, wind, batteries – requires massive amounts of fossil fuel. If political leaders were serious about climate and energy, they’d work together to chart a rational transition path – one that acknowledges that we’ll need fossil fuels for at least another decade to power the shift itself.

Biden never understood that – or didn’t care. His energy policy wasn’t about solving the problem. It was about satisfying a political base with unrealistic promises.

Trump, whatever you think of him, understands the economics of energy. He knows we can’t kill off fossil fuels overnight and expect our economy to keep functioning. Becoming energy independent while continuing to build out smart renewable infrastructure is the only adult path forward – and he seems committed to it.

US Energy Prices Since Jan. 20, 2025

Gasoline

* As of May 2025, the national average price for regular gasoline is approximately $3.26 per gallon, reflecting a decrease from $3.79 a year ago – a nearly 14% drop.

* The US Energy Information Administration (EIA) forecasts an average of $3.10 per gallon for the summer months, marking the lowest inflation-adjusted summer average since 2020.

Natural Gas

* In Jan. 2025, the Henry Hub spot price for natural gas averaged $4.62 per million British thermal units (MMBtu), up from $4.03 in January 2024.

* The EIA projects that natural gas prices will average $3.37 per MMBtu in 2025, a 24% increase from the previous year.

Electricity

* Residential electricity prices are expected to grow by 3% in 2025, the smallest annual increase since 2020, reflecting relatively low natural gas prices and ongoing grid infrastructure improvements.

The Real Costs of Transitioning to Renewable Energy

Lithium-Ion Battery Production

* Producing lithium-ion batteries is energy-intensive. The manufacturing process requires substantial amounts of energy, often derived from fossil fuels, leading to significant greenhouse gas emissions.

* Despite a 90% decline in lithium-ion battery prices since 2010, reaching below $140 per kilowatt-hour in 2023, the environmental and energy costs of production remain considerable.

Electric Vehicle (EV) Infrastructure

* The production of EVs and the establishment of charging infrastructure demand significant energy and resources. For instance, manufacturing EVs involves mining and processing of rare earth metals, which is energy-intensive and environmentally taxing.

* The US energy storage industry has committed $100 billion to develop domestic battery manufacturing, yet experts argue this may be insufficient to build a competitive supply chain from scratch.

Renewable Energy Deployment

* While the cost of renewable energy technologies like wind and solar has decreased, the transition requires substantial upfront investments. For example, the global weighted average Levelized Cost of Electricity (LCOE) for new onshore wind projects was 67% lower than fossil fuel-fired alternatives in 2023.

* However, integrating these technologies into existing grids necessitates additional investments in storage and infrastructure to manage intermittency and ensure reliability.

Success Grade: A-

Effort Grade: A+

Messaging Grade: D

Prices are down, production is up, and for the first time in years, energy policy is being driven by reality, not ideology. It’s a big shift – one that’s already having real-world impact.

But in terms of messaging, Trump isn’t even trying to win over his opponents. Now that he’s back in office with what he views as a clear mandate, he’s not looking to build bridges. He’s looking to rub his critics’ noses in the fact that his policies are working.

Slogans like “Drill, Baby, Drill!” aren’t policy statements – they’re rhetorical jabs meant to antagonize the people who’ve spent the last eight years attacking him, often unfairly. His base loves it. But for the good of the country – and the long-term success of his policies – he might consider dialing it back. Not because his critics deserve kindness, but because victory is more complete when it brings others along with it.

You might think that Trump is not particularly interested in this next issue, but during his campaign he spoke of it a lot and made some significant promises.

Make America Educated Again

Success Grade: TBD

Effort Grade: A

Messaging Grade: B+

As with almost every item on his agenda, Trump has moved quickly to implement his platform on public education. What distinguishes this effort from many others, however, is that he is saying the right things when explaining or defending his actions. He’s made clear where he stands: with parents and against federal micromanagement.

Now to an issue that was already on its way to becoming a non-issue during the campaign. But since it was, in my opinion, a decisive factor in Trump’s dominant win, there was no way he was going to leave it alone after he took office. I’m talking about DEI and trans rights.

Make America Fair and Colorblind Again

What Trump Promised

During the 2024 campaign, Trump spoke repeatedly – sometimes bluntly – about his intention to end what he called the “Wokeification” of government. He tied this goal directly to two issues that had dominated headlines and polarized voters during the Biden years: Diversity, Equity, and Inclusion (DEI) mandates and the transgender rights movement, particularly as they applied to public schools, government hiring, and healthcare policy.

He promised to “ban DEI from the federal government,” defund agencies and departments promoting identity-based hiring, and restore what he called colorblind meritocracy. On the trans front, he vowed to roll back federal guidelines that redefined gender identity in ways many voters found extreme or confusing – particularly in schools, sports, and children’s medicine.

It wasn’t just rhetoric. These issues had become referendums – on common sense, on biology, and on whether the government was still connected to reality.

What He’s Done

Shortly after taking office, Trump issued Executive Order 14094, formally ending all DEI-related hiring mandates and training programs within federal agencies. The order also barred any department from contracting with outside firms that promote race- or gender-based quotas. Several cabinet departments – including Education, Health and Human Services, and the Pentagon – were instructed to audit all internal diversity initiatives and eliminate any found to conflict with “merit-based governance.”

In parallel, he reversed Biden-era guidance that expanded federal definitions of gender identity. He directed agencies to return to biological sex as the legal standard in areas such as school sports, healthcare categorization, and prison housing.

In doing so, Trump effectively made good on his promise – not just to reverse a set of policies, but to signal a reversion to traditional definitions of equality and fairness.

What Biden Did – and Why It Backfired

The Biden administration leaned hard into DEI and trans-rights advocacy. Initially, this seemed like a way to consolidate the progressive base and prove moral leadership. But both issues quickly became liabilities.

The DEI agenda, based on the idea that equity (equal outcomes) should replace equality (equal opportunity), led to widespread public discomfort and distrust – although, because of political correctness, most centrists and liberals would not criticize it. But those that were accusing US culture of structural racism, sexism, misogyny, and transphobia, and advocating DEI as a solution, had no idea that most Americans did not like it. Some may have pretended to be in favor of it, but election results exposed the truth about what common-sense people think about nonsensical ideas.

It’s no exaggeration to say that these issues cost Biden the swing states. And it’s telling that, in the aftermath of Trump’s victory, both have largely disappeared from the public stage. Not because the debates are resolved – but because many of the loudest advocates were never deeply invested. These were ideological bandwagons, not enduring principles.

What It Feels Like

To me, this feels less like a policy reversal and more like a return to national sanity. The DEI and trans policy surge during the Biden years was unsound – not just politically, but economically and scientifically. And, as I said, most Americans, even if they stayed mute on the issue, didn’t like it.

Trump understood how important these issues were to the middle – especially to undecided voters in swing states. He campaigned on reversing them. And then he did. The fact that these issues have now mostly vanished from the media cycle is telling: The movement behind them wasn’t deep. It was performative.

Success Grade: C

Effort Grade: B

Messaging Grade: D

Trump delivered on his promise to eliminate DEI mandates and reverse federal trans policies – but it wasn’t a particularly difficult task, given how unpopular those initiatives had become. He kept his promise, but the political cost was low, and the opposition was already softening.

In terms of messaging, he won the election by articulating what most Americans were afraid to say. But I think he could have done even better – and won over more voters – if he had toned down the negative rhetoric and showed a little love and compassion.

Now we move to four issues that are in some ways the biggest.

Of all Trump’s promises, this next one may have been the most resisted – and the most revealing. “Draining the Swamp” wasn’t just about firing bureaucrats or eliminating inefficiencies. It was about confronting an entrenched system of unaccountable power that had calcified across decades of bipartisan complacency.

Make America Swamp-Free Again

What Trump Promised

“Draining the Swamp” was another popular campaign slogan that Trump used to appeal to his base.

He repeatedly vowed to slash waste, root out fraud, expose corruption, and gut the administrative state.

He called out the “Deep State” directly – unelected officials, agency heads, and career bureaucrats who, he said, acted more like a shadow government than public servants. He promised to bring the bureaucracy to heel, not just through oversight, but through reorganization and, when necessary, demolition.

What He’s Done

Trump jumped on this promise in his first week in office. He created the Dept. of Government Efficiency (DOGE) and made one of the most consequential appointments of his presidency: Elon Musk.

Traditionally, Musk’s job would have been to investigate waste, fraud, and corruption and then to report back to the president and his department heads and let them decide what to do about it.

But Trump wanted to move faster than that, so he gave Musk the authority to not just investigate, but ask questions and audit documents and to some degree (this is not at all clear from anything I’ve read) execute some of his own recommendations.

The response was immediate and strong. Quicker and stronger than I expected. Within minutes after Musk accepted the role, Democrats in Congress, progressive media outlets, and entrenched bureaucrats from dozens of agencies sounded the alarm.

But they had a problem. What politician would be honest enough to say, “Waste, fraud, and corruption? That’s how we get rich!” What editorial board would be willing to argue against a mandate for honesty and efficiency?

They couldn’t attack the mission, so they decided to attack the man. Musk was painted as erratic, egotistical, inexperienced in government. His team of young technocrats – some barely out of graduate school – was mocked as naïve and unqualified. (Fact: They were all highly intelligent, more than well qualified, and thoroughly vetted before they were brought on.)

Despite the daily outrage, accusations, and by then tired claims that Trump was putting an end to Democracy, Musk and his team moved forward. And within a week, they were uncovering hundreds and then thousands of documents revealing hundreds of billions of dollars in misallocated funds, fraudulent contracts, and duplicative programs.

As each of these discoveries were made, they were posted to a public website that Musk put up so that the public could see exactly what DOGE was doing. Here’s just a small sample of what they found:

* Tens of billions in recurring “emergency” funds for agencies whose missions hadn’t changed in 20 years.

* Ghost employees and shadow contractors drawing full federal salaries without any verifiable output.

* Duplicated programs across multiple agencies – each with its own staff, budget, and lobbyists.

* Deep financial entanglements between regulatory agencies and the very industries they were tasked with overseeing, including Big Pharma, defense contractors, and agricultural giants.

At one point, Musk said his goal was to identify $1 trillion in waste. He didn’t hit that number before stepping down from active DOGE leadership, but what he uncovered during his time as director was so massive and so shocking that it’s hard to believe the total cost to taxpayers wasn’t at least $1 trillion a year.

Indeed, by the end of April verified DOGE documentation showed $618 billion in confirmed waste, fraud, and abuse – with at least another $300 billion still under review.

Meanwhile, progressive leaders were accusing Musk of authoritarian overreach. Mainstream media figures painted Musk’s reforms and recommendations as callous and disingenuous attempts to enrich himself at the expense of “ordinary voters.” DOGE was just one more attempt by Trump to replace America’s democratic institutions with a ruling class of billionaires.

And it was not just progressives or even just Democrats that were opposing DOGE. Opposition came from Republicans, Independents, and even some Libertarians.

As the anti-Musk vitriol got louder and more focused, Tesla became a political symbol for both sides of the aisle. There were arguments on both sides, but the violence and vandalism came almost entirely from the left.

There were Tesla boycotts. Vandalism. Even firebombing of Tesla cars – acts of political violence aimed not at protest, but intimidation. But neither Musk nor Trump backed down.

What It Feels Like

I’ve always that believed government waste was real. But I used to think it was mostly due to bureaucracy, DEI-type standards, and incompetence stemming from a lack of giving-a-shite. Watching the DOGE Show play out changed my mind. The backlash wasn’t bureaucratic inertia – it was politicians, lobbyists, government contractors, and bureaucrats joined together in a common effort to protect their scams.

Presidents have talked for decades about making government smaller and more efficient. But I believe this is the first time it was being tried in earnest.

Musk didn’t just shine a light on government waste and inefficiency. He exposed a vast, interconnected system employing, directly and indirectly, millions of people working on programs and projects that, for the most part, our country doesn’t need, including some that were outright damaging to our economic strength and, yes, our damned democracy!

Musk’s willingness to lead DOGE and to endure, without complaint, the undeserved and vitriolic criticism he got for it – not to mention the $100 billion he lost in net worth as a result of the threats and criminal acts made against Tesla – makes him, in my eyes, nothing less than the greatest American patriot alive today.

Success Grade: TBD

Effort Grade: A+

Messaging Grade: C+

It remains to be seen whether DOGE will survive and finish what it started. But finally, after decades and decades of presidential promises to get rid of government waste and corruption, someone – actually, two people – were willing to give it a try.

Okay, we are getting to the final three – starting with Trump’s pledge to change a century of American trade policy by instituting reciprocal tariffs against countries that “have been ripping off America for years.”

Make International Trade Fair Again

What Trump Promised

Trade was one of the few issues where Trump clashed head-on with traditional conservatives – and he made no apologies for it. Throughout his 2024 campaign, he repeated a simple message: America gets ripped off.

He claimed that China, Europe, and other major trading partners had taken advantage of US economic openness for decades – flooding the market with cheap goods while keeping their own barriers high.

He vowed to change that, promising a new policy of reciprocal tariffs: If a country put tariffs or quotas on American goods, the US would do the same. And if a country wanted truly free trade, with zero tariffs on both sides, Trump said he’d welcome it.

Although he said so rarely during the campaign, since he’s begun imposing tariffs, he’s been providing another argument for what he’s doing. His goal, he now says, wasn’t protectionism – it was leverage. His best scenario result, he’s saying, is what he thinks of as real free marketing trading with zero tariffs on both sides.

What He’s Done

In his first 100 days, Trump:

* Imposed a new round of targeted tariffs on Chinese steel, electric vehicles, and solar panels.

* Warned European automakers of pending tariffs unless the EU eliminates its own vehicle import duties.

* Pressured Mexico and Canada to renegotiate certain provisions of the USMCA that he claims are being “quietly gamed.”

* Called for a 10% universal baseline tariff on all imports from countries that don’t offer equivalent market access to the US.

* Reopened trade negotiations with Japan, Italy, and Brazil – each of which reportedly expressed interest in bilateral “zero-for-zero” deals: full tariff elimination on both sides.

As a political strategy, Trump’s tariff promise was imperfect at best.

It appealed to some portions of US industry and commerce – the companies that could not possibly compete with their overseas competitors. But businesses that build their products in China and companies that buy product components from China would not be happy with the US government imposing tariffs where there were none before or raising tariffs because that would force them to pass that extra cost to the consumer by way of higher prices, and that might reduce the demand for what they sell.

The strategy would also be unpopular with all the foreign countries that would be affected by such tariffs and their US partners and lobbyists who understandably benefit from our long history of charging no tariffs on products from countries that impose tariffs on US goods selling to their markets.

Trump himself acknowledged that there would be “some pain” during the negotiations, but insisted that if Americans were patient, he’d get them their cake and let them eat it too.

We are in that period of pain now, with prices rising on many imported products and many small business owners predicting that they will soon have to close shop if Trump can’t get to a reciprocal zero-tariff deal very soon.

In pursuing this agenda – an agenda that he has advocated for decades, by the way – Trump has encountered broader opposition than for any of his other campaign promises. When it comes to Classical Liberals and Libertarians, Trump’s tariff policies are downright stupid. And my colleagues who share these perspectives have not been shy about saying so.

As with his other campaign promises, the opposition Trump is facing now has not deterred him. Notwithstanding several temporary concessions on the tariffs he initially imposed, he seems intent on pursuing this strategy as far as he can.

What It Feels Like

As I said, most of my Libertarian friends – and more than a few of my conservative ones – think Trump’s trade policies are both ill-conceived and bad for the economy.

What’s interesting is that all my liberal friends agree! Few of them can explain why they are bad except to mimic what they’ve heard other liberals say: “Tariffs make everything more expensive. The cost of the tariffs is passed through the companies that pay them to the consumers.”

And that is mostly true.

But Trump’s trade and tariff policies must be judged by their intent. In other words: What’s the goal here?

Because if Trump is right – and admittedly, that’s a big if – his tariff scheme could result in more free trade and, thus, lower prices.

What Trump’s tariff strategy can’t do is what he is promising now. It cannot produce both lower prices and more income to the government that it can use to lower taxes on middle-class Americans. Or, if it can, it’s beyond my understanding of economics. He’ll have to explain how that can work.

In terms of achieving two-way free trade, Trump’s deal making does seem to be making progress. At least three major nations are reportedly exploring zero-for-zero deals. That wouldn’t have happened without pressure.

But whether this approach succeeds or collapses into tit-for-tat retaliation remains to be seen. It’s not a completed policy. It’s a gamble in progress.

Success Grade: TBD

Effort Grade: A+

Messaging Grade: B+

Trump hit the ground running and clearly means business. He’s pursuing his idea of “trade fairness” the only way he knows how: hard.

But the strategy will only succeed if he is able to persuade not just individual countries but the European economic zone and, ultimately, China as well.

Meanwhile, he does seem to be trying to get his message heard, and I give him props for that. But he has so much of the world against him on this issue that I’ll be shocked if he succeeds.

Since we are talking about global relations, let’s look at what Trump promised to do on the broader stage of foreign affairs.

Make America Great Again – Abroad

What Trump Promised

Of all Trump’s promises, this may have been the most ambitious: to remake American foreign policy – to disengage from endless wars, stop subsidizing allies who freeload, and put American interests ahead of vague global ideals.

It won’t surprise you to know that I’m not an expert – nor do I consider myself to be an expert – in foreign relations, national defense, global diplomacy, or international trade. I haven’t worked in think tanks or briefed presidents. But, like millions of other Americans, I’ve followed these issues with interest over many years. And I believe I’ve developed a reasonably accurate sense of what’s going on – and what’s good for America.

That’s not nothing.

Because whether or not you’re an “expert,” having opinions about global politics today feels almost like a civic duty. So, while I’m aware that there’s nuance and complexity here, I’ll say what I think – and I’ll try to say it with a little humility.

Trump’s critics like to paint him as reckless or simplistic when it comes to foreign affairs. But the truth is, he has an underlying view of the world that’s more coherent than they admit. It’s not ideologically isolationist, nor is it neoconservative hawkish. It’s fundamentally pragmatic – and instinctively anti-war.

Trump sees war as expensive and destructive. He doesn’t reject it on moral grounds – he’s not a pacifist – but on practical ones. He’s not afraid to use military force if he believes there’s a serious, imminent threat to American lives. But he sees little sense in using our blood and treasure to fight proxy wars that don’t serve American interests. That’s why he was, and still is, deeply skeptical of the war in Ukraine, just as he was about our involvement in Iraq and Afghanistan.

He’s also right, in my view, to be far more wary of Islamist extremism than of Russia. The cultural values, long-term goals, and ideological rigidity of Islamic fundamentalist movements are more alien – and more hostile – to the American way of life than anything Putin is peddling. It’s not fashionable to say this, but it’s true.

Trump’s broader foreign policy message is that America should lead with leverage, not with lectures. And that’s worth taking seriously.

What He’s Done

Much of Trump’s second-term foreign policy is still taking shape, but the broad strokes are familiar. In his first 100 days, he has:

* Renewed pressure on NATO countries to meet the 2% GDP defense spending target – this time making it clear that there will be penalties if they don’t.

* Halted new military aid to Ukraine and ordered a full audit of past US defense and financial transfers.

* Slashed US contributions to international climate and development programs, including UN and WHO initiatives.

* Launched back-channel diplomacy with Russia, Iran, and North Korea.

* Reopened trade negotiations with Japan and several European nations with the goal of reaching more balanced reciprocal deals.

He’s also reopened disputes with Canada over defense cooperation, and – yes – brought up Greenland again. But those who see this as erratic behavior miss the deeper pattern.

Trump often opens negotiations with provocative gestures or statements. They’re not random. They’re intentional. His goal isn’t to shock people for its own sake – it’s to disorient the opposing party and reframe the terms of the discussion. It’s a real estate tactic adapted to global politics.

Is it risky? Of course. But it’s not irrational.

The US has been playing global cop for decades. We’ve carried the heaviest load in NATO, the UN, and virtually every multilateral institution. We’ve spent trillions trying to stabilize countries and regions that neither love us nor thank us for it. And we’ve propped up an entire global order that allows other nations to focus inward while we pay the bills.

Trump’s foreign policy represents a challenge to all of that. He isn’t trying to destroy the Western alliance system. He’s trying to reset it. He’s trying to say: We’ll do our part, but no more than our fair share.

What he’s not doing – contrary to what many claim – is retreating from the world. He’s still talking to world leaders. He’s still engaged in trade negotiations. He’s still investing in defense. But he is not apologizing, virtue-signaling, or lecturing other nations while asking for nothing in return.

That’s not weakness. That’s a shift in posture.

And it’s about time.

What It Feels Like

It feels like Trump has a notion. Not really a plan. I don’t think he’s thought that deeply about it because it’s never been a realistic possibility.

But now that he has momentum, I expect that he’ll keep pushing this agenda forward. And now that he has talent and loyalty in the federal agencies, it seems likely he will have some success. Not all that he says he wants, but maybe all that he’s hoping to get.

Success Grade: TBD

Effort Grade: A

Messaging Grade: B

Trump’s foreign policy is aggressive, unapologetic, and one-dimensional. There is no reason to hope that he will win this battle on every field, but I’d be surprised if he doesn’t score at least a half-dozen solid victories. And as far as I can see, that feels like a good thing.

NATO Defense Spending – Who Pays What?

As of 2024, NATO comprises 32 member countries, each committed to spending at least 2% of their Gross Domestic Product (GDP) on defense. This benchmark was established to ensure equitable burden-sharing among allies.

Key Statistics

United States

* Defense Spending: $967 billion

* Percentage of GDP: 3.37%

* Share of NATO’s Total Defense Spending: Approximately 68%

Poland

* Defense Spending: $34.98 billion

* Percentage of GDP: 4.12%

United Kingdom

* Defense Spending: $82.11 billion

* Percentage of GDP: 2.33%

Germany

* Defense Spending: $22.78 billion

* Percentage of GDP: 2.09%

France

* Defense Spending: $64.27 billion

* Percentage of GDP: 2.06%

Canada

* Defense Spending: $34.98 billion

* Percentage of GDP: 1.55%

In 2024, 23 NATO members met or exceeded the 2% GDP defense spending target, a significant increase from only three members in 2014.

US Contributions to the UN and Climate Funds

The United States has historically been the largest financial contributor to the United Nations (UN) and various international climate initiatives.

UN Contributions

* Regular Budget: The US is assessed to contribute 22% of the UN’s regular budget.

* Peacekeeping Operations: The US is assessed to contribute 27% of the UN’s peacekeeping budget. However, US law caps its peacekeeping contributions at 25%, leading to accumulated arrears.

Climate Finance

Green Climate Fund (GCF): Between 2014 and 2024, the US contributed approximately $2 billion to the GCF. In contrast, during the same period, Congress approved at least $79 billion in foreign military financing, highlighting a disparity between military aid and climate finance.

With that, we come to our last issue: a promise Trump made that, I must admit, I thought he could do and right away. That hasn’t been the case, but I’m still optimistic he’ll get it done before things spiral out of control.

Make America Peaceful Again

What Trump Promised

Throughout his 2024 campaign, Trump promised to end the war in Ukraine as soon as he took office. At one point, he stepped up the pledge, claiming he would end the war in Ukraine “before I even take office.”

At rallies, in interviews, and during the debates, he framed the war as a preventable catastrophe prolonged by US interference and bad diplomacy. He claimed the Biden administration’s foreign policy had all but started the war, and then intensified it to the point where it could escalate hugely.

He never said how he would end the war, but I believe lots of observers, including yours truly, knew what he was thinking. And I believe that those that were supporting Ukraine – in Congress, in the media, and in the military – knew, too. That is why there was so much opposition to his claims – even though, in terms of public awareness, no one knew anything.

What He’s Done

Even before Trump took office on Jan. 20, he was working on his “secret” plan. He was having confidential conversations with Vladimir Putin, presumably to get a feel for his temperature generally and to feel out what he might think of Trump’s “solution.”

After taking office, he did several significant things. He paused all new US military aid to Ukraine. He ordered a full audit of weapons shipments and financial transfers made under Biden. And he made it clear, both publicly and through back-channel diplomacy, that continued US support would depend on Ukraine’s willingness to negotiate a ceasefire.

In February, he sent a delegation to meet with both Russian and Ukrainian intermediaries in Istanbul. While the talks were not officially acknowledged by the White House, several outlets – including The Wall Street Journal and The Times of London – reported that a framework for a provisional ceasefire was being discussed.

The White House neither confirmed nor denied this, but Trump later tweeted, “The war would be over already if not for the warmongers in DC and Brussels. We’re still working to bring both sides to their senses.”

What he was referring to was (in my opinion) the opposition he was facing from the “Deep State” – i.e., the Democrats and neocon Republicans that wanted the war to continue by boosting US support for Ukraine. Trump ran into the entrenched power of what President Eisenhower dubbed the “Military-Industrial Complex.” It was larger and stronger than he had imagined.

Trump believed, rightly I think, that Russia invaded Ukraine because the Biden administration had signaled that they would support a Ukrainian bid for NATO membership. This would have put the potential of ICBMs and even nuclear weapons on Russia’s border, dramatically increasing the danger of NATO’s core purpose, which was always to stand against Russia.

Ukraine’s bid to join NATO had been going on during Trump’s first term, but it didn’t go anywhere because the key players knew that Trump wasn’t happy with NATO. And I believe that Trump had promised Putin that so long as he (Trump) was president, it wouldn’t happen.

The neocons and Democrats that see Russia as a great threat to the US (or simply like the financial benefits the Military-Industrial Complex gets from continuing the Cold War) called Trump’s strategy “naïve,” and said it would undermine the existing deterrence against Russian ambitions and reward Putin for his invasion.

Meanwhile, the war continued and US political, media, and popular support for Ukraine grew. This emboldened Ukrainian President Zelensky, who doubled down on his position of giving up nothing to the Russians.

Despite almost universal condemnation against Trump’s policy among Democrat politicians and the mainstream, Trump continued his efforts to strike a deal by negotiating with Putin on what terms he was willing to agree to while pressuring Zelensky to accept terms that were less than he wanted.

There are obviously no public statements available about what those terms could be, but my guess is that, for Russia, they included a guarantee that Ukraine would not join NATO, as well as the acquisition of a slice of Ukraine, probably the Crimea. I say that because I don’t think Putin will be satisfied with just a promise about NATO. He must want something tangible, such as a strip of land along the border or access to the sea, to provide the protection from future threats that he now sees as probable.

My prediction is that unless Putin gets what he wants (not what he’s asking), the war won’t stop. And Donald Trump wants the war to stop. He wants it theoretically because he has always recognized the cost of war. And he wants it practically because he wants to be seen as the president that could do what Biden could not.

At this point, it’s hard to know what the outcome will be. Zelensky has agreed to Trump’s demand for mineral rights. And there are indications that he might be softening his no-compromise position on a peace deal. (Russian Foreign Minister Sergei Lavrov, in turn, said that Moscow would consider “new proposals from the Americans” if they were presented seriously.)

On the other hand, the closer Putin comes to getting what he wants, the more he will be tempted to see if he can get that much more – which is why I think we’ve seen Trump’s recent chastisements of him.

The current bottom line: No peace deal has been announced. No ceasefire has been signed. But there’s movement – more than we’ve seen in nearly a year.

What It Feels Like

Trump said he’d end the war in Ukraine pronto. He hasn’t. But he’s taken visible steps in that direction. His critics argue that he’s caving in to Putin and that he’s weakening NATO unity and giving Putin leverage. But those that understand what’s at stake want this battle of the Cold War to continue. So, they will say anything they can think of to foil his efforts.

But as I said, Trump is a different president today than he was in 2016. He’s not concerned about his detractors. He’s dead set on doing what he wants to do.

I hardly feel good about the status of this war, but I do have some hope that Trump can succeed because it is in the best interests of Russia and Ukraine and the US to make peace. If Trump walks away from his role now, Putin may very well accelerate and intensify Russia’s assault on Ukraine. And that will be bad for everyone –especially Ukraine.

Success Grade: B- so far

Effort Grade: A+

Messaging Grade: B

Trump hasn’t ended the war, but he’s made a real effort to shift its trajectory. Whether that effort succeeds remains to be seen – but it’s too serious to dismiss.

Final Grade: The Long View

At the end of Trump’s first 100 days back in office, a lot remains “TBD.” Many of the most significant promises – ending the Ukraine war, reforming the Dept. of Justice, slashing the Deep State, and negotiating new trade deals – are in motion but far from resolved. Even on easier wins like declassifying the JFK and Epstein files and sealing the border, we’re still waiting for real follow-through.

That said, looking at the campaign promises Trump is attempting to keep right now, it’s clear to me that no US President in my lifetime has tried to do so much, so fast.

Think about it.

Reagan’s first 100 days were mostly setup. Obama passed a stimulus bill and proposed a healthcare plan, but the first failed and, though the second passed, it was only one dubious achievement. Biden signed a string of executive orders – most of them reversals of Trump’s 2016 policies – but those that had any bite at all were negative for the economy, slowed GDP growth, and stimulated inflation.

I think you’d have to go back to FDR and his “New Deal” to find the breadth and depth of change that Trump’s first 100 days are on the verge of creating. But even FDR limited the scope of his ambitions to his major challenge: Depression-era economic legislation.

In this report card, I gave solid marks to Trump where progress is measurable – e.g., the border wall, deregulation, parental rights, and tariff policy. I gave lower marks where results are questionable or still pending – e.g., foreign policy initiatives and cultural reset promises.

So, what’s the final grade?

It’s not possible to give Trump a final grade at this point because, notwithstanding 100 days of unprecedented action, his agenda, however enormous, is mostly a grand ambition.

There are too many open questions and too many battles left to win. But for sheer determination, early energy, and the willingness to go to war on promises most politicians would water down or walk back, I’d say he has put himself in a position where he could be, if he is smart and the chips fall in his favor, what Nancy Pelosi used to say about Biden (to her embarrassment): the “most consequential president” of the last 100 years.