In the past two weeks, I’ve read at least a dozen essays and articles about Trump’s campaign against the raison d’etre of the Federal Reserve (which makes great sense to me) and his recent campaign to get the Fed to lower the rate. The betting was that they would bring it down but by, at best, half a point. Well, they did. They brought it down 250 basis points (one-quarter of a point) and I figured that was a compromise that probably wouldn’t have an effect on the economy one way or the other. Yesterday, I came across two good pieces that challenged my assumption. The first suggests that gold might be a way to deal with or profit from Trump’s campaign. The second provides four alternatives that are stocks. – MF

Three Good Reasons You Should Not Buy Gold Now…

and One Good Reason You Should

From Ashwin Thapar, D.E. Shaw Investment Management

“Here are some good reasons not to invest in gold. First, it earns no dividends or interest. Second, you can’t live in it, like real estate. Third, it has doubled in the past few years, so forget about buying at the bottom.

“Nonetheless, a prudent, diversified investor should consider owning gold today. This isn’t about potential return. It is about insurance. Gold tends to go up when bad things happen, from inflation and runaway government debt to war and political instability. Those things seem more likely now than they have for a long time.

“In a new report, Ashwin Thapar, of D.E. Shaw Investment Management, argues that as global wealth grows, so should gold holdings. He estimates that since 1975, gold has ranged from 1.8% to 7.3% of developed market liquid wealth. (It has recently broken above that range.)

“Newly mined gold increases the stock of gold less than 2% a year, according to JPMorgan Chase. The remainder of gold wealth comes from a rising price. Over the long run that is probably enough to keep up with Treasury bills, but not a plain vanilla mix of stocks and bonds. The purpose of gold is to damp the impact when something hammers stocks, bonds, or the dollar. The trick is to figure out what that something is.

Inflation: Gold’s Best Friend

“Gold does best when fiat currencies (the kind central banks issue) lose purchasing power. Gold soared during the 1970s as stocks and bonds foundered amid double-digit inflation.

“US inflation, at around 3%, is hardly a disaster. And the Federal Reserve thinks it will be lower in a year in part because of a weaker labor market, which is why it is likely to trim interest rates on Wednesday. [Note: It did. See Porter Stansberry’s piece, below. – MF]

“But the structural forces that kept inflation below the Fed’s 2% target before 2020 have switched direction. Globalization, which brought a flood of low-cost goods to American shores, is out; tariffs, protection and reshoring are in. Before, legal and illegal immigration compensated for an aging labor force. That inflow has been. Cut off even as fertility rates hit new lows.

“These structural pressures need not push inflation higher. The Fed can ensure inflation stays low by raising the real interest rate (the nominal rate minus inflation), which weakens demand and pricing power. As D.E. Shaw points out, higher real rates are bad for gold.

“But making such tough decisions requires the Fed to remain independent. And before long, it may not be. President Trump told reporters the Fed should be independent, ‘but I think they should listen to smart people like me.’

“He is taking unprecedented steps to ensure the Fed listens. He has just installed the chairman of his Council of Economic Advisers, Stephen Miran, as a Fed governor. Miran will retain his White House title while on the Fed. Trump is also trying to fire another governor for alleged mortgage fraud. By next May, he can replace Chair Jerome Powell. He is forthright about his goal: Get interest rates down faster.

“Investors don’t seem to think this will lead to higher long-run inflation, and they might be right. But an end to Central bank independence is the sort of once-in-a generation risk investors struggle to price, and for which gold is well-suited.

Stocks and Bonds

“When interest rates go up, bond prices go down, and gold usually rises. So gold can hedge bonds. But that hedging value depends importantly on why interest rates are going up. In low inflation eras, rates rise and bond prices fall because of better economic prospects, and stocks rally. So stock and bond returns are negatively correlated, and hedge each other.

“But at times of rising inflation, bond and stock prices rise and fall together. Their returns are positively correlated and no longer hedge each other. This makes gold even more attractive, because it can hedge both. There are signs of this now.

“You could hedge against inflation with Treasury inflation-protected securities, or TIPS. But last month, Trump fired the commissioner of the Bureau of Labor Statistics after it reported unflattering jobs data, and nominated a partisan supporter to replace her. Investors must now weigh the risk the BLS will change the consumer-price index to lower reported inflation. That would undercut the protection offered by TIPS, which are indexed to the CPI. Gold isn’t.

Debt and the Dollar

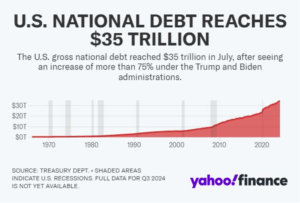

“The publicly held federal debt is on track to rise from almost 100% of gross domestic product now to 120%, exceeding the all-time high during World War II, according to the Committee for a Responsible Federal Budget. Neither political party has a credible plan to stop the rise.

“High debt poses two risks, both of which make gold attractive. The more remote is that the government defaults. The other is ‘fiscal dominance,’ in which the central bank gives priority to keeping the federal debt burden manageable over inflation. Indeed, Trump regularly cites debt costs as a reason why the Fed should cut rates.

“Gold also competes with the dollar as a reserve asset for central banks, sovereign-wealth funds and individuals trapped in kleptocratic regimes. The dollar, however, has lost some of its reserve appeal since early 2022, when Western governments froze Russia’s foreign-exchange reserves because of its full-scale invasion of Ukraine. Goldman Sachs estimates central bank buying accounts for most of gold’s doubling in price since. Trump’s trade war this year further soured investors on the dollar, no doubt helping gold.

“If high inflation, fiscal dominance or a loss of reserve status threaten the dollar, you could buy foreign currencies. But other countries also have high debt and political instability. You can’t be sure the euro will exist in a decade, given the rise of euroskeptic parties in Germany and France. Gold hedges against a collective loss of trust in fiat currencies.

Gold as Insurance

“Fear of inflation, fiscal dominance, dollar depreciation, war and political instability are why gold has already risen so much. Since these risks are already reflected in its price, why buy now? This argument sounds like what you hear at the top of a market.

“The case for gold doesn’t depend on where its price is going, but its role in your total portfolio. According to D.E. Shaw, someone optimizing both return and risk might allocate anywhere from 0.5% to 9% of a portfolio to gold. The share is higher when stocks and bonds are positively correlated, or a financial disaster, such a stock market crash or inflation spike, are a concern. This allocation isn’t right for everyone; it depends on personal risk tolerances.

“And what if your gold goes down? Think of it as an unused insurance policy. And be glad your house didn’t burn down.”

Investing in This Post-Rate-Cut Economy

From Porter Stansberry

“Rate cuts just might ignite a fire.

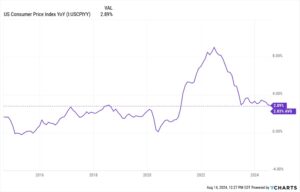

“US gross domestic product (GDP) grew 3.3% in Q2. The current unemployment rate is 4.3%. And the latest consumer price index (CPI) showed prices are rising at close to 3% year-over-year. All of this points to a tight economy with little slack.

“And 3% inflation is nowhere near the 2% rate that the Federal Reserve has officially targeted.

“Further, many analysts believe the full effects of the Trump administration’s tariff policies have yet to fully feed into the CPI reports. That means inflation could potentially accelerate in the coming months.

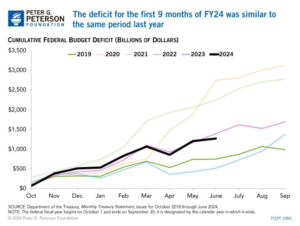

“And despite all the promises about Elon Musk and the Department Of Government Efficiency (DOGE) cutting the federal budget, government spending continues to run completely out of control.

“So, given that backdrop, of course the Federal Reserve has decided to… cut interest rates – reducing the Fed funds rate 25 basis points to around 4.25% from 4.50% – and hinting at more to come later this year. As irresponsible as this might seem, this is the current state of affairs.

“Adding liquidity to financial markets in this economic environment is akin to throwing a match on a towering inferno. Gold, one of the clearest barometers of inflationary pressures, has taken another leg up in the last month to yet another all-time high at nearly $3,700 per ounce. Hard assets are sending a very clear signal that inflation is not going away.

“While it might seem like party time for stocks, investors should be wary.

“So far, the reflexive reaction to Fed cuts has been for longer-term US bond rates to fall. The 10-year yield has now dipped from around 4.3% a month ago to just above 4.0%. That is pretty close to panic lows hit immediately after Liberation Day, when on April 2, President Donald Trump announced his tariff plans, and about the lowest levels in close to a year. But the last chapter on this has yet to have been written.

“It isn’t clear why financial markets will just give the US a pass and allow the government to fund such recklessness at lower rates. In fact, if inflation picks up – as gold is signaling – and government spending continues unabated, it seems possible that longer-term rates will end up higher after the Fed executes its series of rate reductions, not lower. That would likely act as a shock to equity prices and force a potentially significant market correction.

“And that would leave the Federal Reserve with no good options.

“So what is an investor to do in such an environment? Certainly, continue to focus on gold and other hard assets that perform well in an inflationary backdrop. And look for equities with strong cash flow, good balance sheets, and high-quality businesses that can thrive even in a volatile economic environment.”

Note: If you’d like to hear more from Porter, he has a free advisory called The Big Secret on Wall Street, which is currently recommending four stocks that he thinks will perform well in the future, despite these economic uncertainties. One is a leader in health and wellness that continues to capitalize on its loyal following. Another is an energy-drink powerhouse in the midst of a potentially transformative acquisition. There is more feedback on a company taking the industry reins in weight-loss drugs. And finally, a value story in the energy space that looks to have dodged a political bullet. Click here to subscribe to The Big Secret on Wall Street and read the full issue.

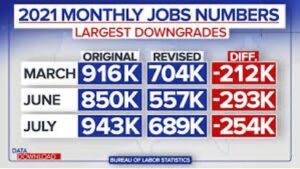

David Stockman on the Recent Jobs Report

A recent government report on US employment numbers included the surprising fact that state and local school authorities hired an additional 64,000 teachers and administrators in June. In June! When school lets out! And that number accounted for 44% if the entire gain of 147,000, which was heralded as a great achievement and a meaningful reason to believe the US economy was robust and growing. However, as David Stockman pointed out in an article I read last week (I don’t remember when it was published, but it doesn’t matter), there were hints in that same job report that notwithstanding Washington’s best efforts, America is not spending, borrowing, and printing its way to prosperity after all. It turns out that fully 144,00 or 98% of the alleged “new jobs” reported for the month were in government, including education (73,000), private health and education services (51,000,) and Hospitality & Leisure services (20,000). Here is his take on all that… – MF

“All the new jobs are either funded by government spending, entitlements or tax subsidies like in Medicare and employer health plans, respectively; or they amount to low-wage, part-time, low-productivity jobs in restaurant kitchens and hotel room-cleaning operations.

“This underscores the significance of that, it might also be noted that on the other end of the economy in the goods-producing sectors where the high-pay, high-productivity jobs are located, the gain was only a tiny 6,000….

“If we look at the entire past year, we see that these same three sectors, which accounted for 98% of the new” jobs this month, also accounted for 1.492 million or 82% of the total job gains of 1.809 million since June 2024….

“There is nothing new about this pattern….

“Ever since the turn of the century the US economy has been churning out modest overall labor utilization gains… with the index of aggregate hours worked for the entire private sector up by only 0.72% over the last 25 years….

“[And for the past quarter century, those have mostly been] in the government-funded health, education and social services sector and the bars, restaurants, hotels and entertainment venues they frequent outside of working hours….

“During this same 25-year period in which total private sector labor hours rose by just 19.5%, the net worth of the top 1% rose by 327%, the Federal debt increased by 537% and the Fed’s balance sheet exploded by 1,100%….

“[In other words, while] while the Fed was running the printing presses at white hot speeds over the last quarter century, the main street economy suffered a 15% loss of its high-pay, high value-added jobs. In turn, that gap was back-filled by jobs largely attributed to government spending, meaning that the simulacrum of a growing labor market was fueled by the proceeds of public sector taxation or borrowing….

“The Fed’s printing press have been running at double digit rates for the past quarter century yet the high pay, high productivity sectors of the labor market have actually been inflated away and off-shored owing to America’s high, uncompetitive cost structure resulting from the Fed’s pro-inflation policies.

“And yet and yet. Here we are again with both Wall Street and Washington clamoring for a new round of ultra-low interest rates and printing press inflation. In the spirit of Einstein’s famous definition of insanity – doing the same thing over and over and expecting a different outcome – it might be wondered as to what will it take for both ends of the Acela Corridor and both wings of the UniParty to grasp the obvious?

“To wit, the trend level of inflation is now stuck smack on 3.0% per annum, as has been posted month and months by the steady 16% trimmed mean CPI, while for all practical purposes rates in the Fed pegged overnight money markets stand at 4%.

“So where in the hell is it written in the economic texts – Keynesian, supply side, monetarist or eclectic – that an advanced industrial economy can’t stand real rates of 1.0%?”